What's New -Aug 2026

Posted Thursday, July 30, 2026

Sales

-

Feature: Prevent Finalizing Deals with Unpaid Down Payments

To ensure your accounting remains accurate and complete, we’ve added a new safeguard for finalizing deals. When enabled, the system will prevent a deal from being set to "FINAL" status if there is an outstanding balance on the received down payment.

- How to enable: Navigate to Settings > Defaults and set Line 13 – Reg DP Rcv's for Final to Yes.

Once enabled, the system will trigger a prompt if a user attempts to finalize a deal with an unpaid down payment balance, ensuring that all funds are collected before closing the deal. Deferred down payments are excluded from this rule. Deals can be finalized as long as there’s no balance on the cash down payment line.

- New Security Controls: Due Bill Management

We have added two new security items for the Sales/F&I Due Bills tab to give management better control over record updates:

- #951 - Edit Due Bill: Allows staff to add or remove items on an individual sale.

- #953 - Edit Due Bill Defaults: Controls access to the "Default Due Bill" lines.

This update allows you to grant your sales team the ability to manage due bills for specific deals without giving them permission to change or edit the foundational Default Due Bill information.

- Enhancement: Automated Commission Splits for Sales Teams

We’ve updated the Sales/Recap tab to streamline commission calculations for multi-person teams. If multiple team members share the same title, the system will now automatically apply commission splits based on the configuration in Defaults > Sales Defaults (Line 34 - Auto Split Commission). This update ensures consistent and accurate commission distribution across your sales and management teams.

Contracts

-

LAW®553-SC(5P) 8/26 and LAW®553-SC-ARB 8/26

Please note that there has been a revision made to the LAW®553-SC(5P)8/24 contract as well as the

LAW®553-SC-ARB8/24. The new form numbers are LAW®553-SC(5P)8/26 and LAW®553-SC-ARB8/26.

Effective July 1st, 2026, the maximum allowable late charge amount has increased from $25.50 to $27.00, and the minimum late charge increased from $10.20 to $10.80. We modified the Late Charge section to reflect the new amounts.

Inventory

-

Improved Inventory Detail View

We have enhanced the "Floored By" label (line 62) in the Inventory tab.

When hovering over this label, you will now see details for all associated floorings—even when multiple records exist. The tooltip now displays the following information for each flooring:

- Flooring company name

- Amount

- Date

- Current balance

Accoutning

-

We are constantly working to improve your workflow in ASN Software. Based on your feedback, we added the ability to change the Bank Reconciliation date, giving you more control over your records.

What’s Changing?

You now have the flexibility to edit the date on your bank reconciliations!

If you need to adjust a reconciliation date, you can now do so as long as:

- The reconciliation is unlocked: You must have an unlocked status to make changes.

- The date is within range: You can update the date freely, provided it is not set to a future month and is not earlier than the date currently selected.

Why does this matter?

We know that accounting adjustments happen. This update allows you to correct dates on pending reconciliations without needing to delete and recreate them, saving you valuable time during your month-end process.

Reports

-

New Reporting Field: Track Lender Funding Speed

We’ve added the Funding_DaysUntilFunded field to our custom reporting tool. You can now create custom reports that calculate the average days to funding for your financed deals. Use this data to effectively evaluate lender performance and identify opportunities to speed up your funding process.

- New Reporting Field: Audit Sales Activity

We have added the MostRecentLedgerTransaction field to the Reports > Custom Reports > Sale List data source.

This field mirrors the "Time Created/Edited" timestamp found in the Accounting/Ledger tab, allowing you to easily track the latest updates to your sales records. This addition is designed to support more accurate auditing and oversight of your sales activities in your custom reports

-

New Feature: Warranty Replacement Parts LOT Filter For Returns

To better support service shops operating across multiple locations, we have introduced a new LOT filter in the return tab for Warranty replacement parts.

If your staff has access to multiple lots, they can now use this filter to quickly locate and manage returns specific to each location. This update streamlines tracking and improves organization for multi-site operations.

- New Security Feature: Restrict Deleting Returns

We have added a new security item (#951) to give management greater control over inventory returns.

You can now restrict shop staff from deleting returns while still allowing them to create new ones. By configuring this new security setting, you can ensure that the ability to delete return records remains limited to authorized personnel.

This update helps maintain better oversight and data integrity within your system. To enable this restriction, please review your security settings for item #951.

- New Feature: Sublet Markup Defaults

You can now automate markups for sublet line items in your repair orders, matching the functionality currently available for parts, labor, and fees.

To configure this setting, navigate to Settings > Defaults > Shop Defaults and enter your desired markup percentage. This addition helps ensure consistent pricing across all service line items.

Software Tip:

Keep Your Credit Disclosure Current

If you need to print the credit disclosure from the Contracts screen, make sure the credit report being used is the most current one. An older credit report may become stale, making the disclosure no longer relevant.

If you've pulled a newer credit report, go to the Credit tab, highlight the most recent report, and click Prefer. This ensures the system uses the latest credit report when generating the credit disclosure on the Contracts screen.

-

The Upcoming version is 7.0.19.29 —Our newest update is rolling out in phases. If you don’t see it yet, no action is needed; it will arrive automatically. Once updated, you’ll have access to the latest features and improvements to keep your system running at its best.

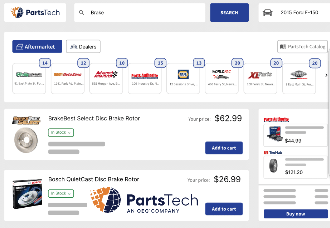

ASN: PartsTech Parts Lookup & Ordering Now Available

Posted Thursday, July 30, 2026

ASN continues to add tools that help make your shop more efficient. We’re excited to announce that PartsTech is now integrated into the ASN Shop Management System, giving service shops a faster and easier way to search for and order parts.

If your shop uses the ASN Shop Management System, you'll notice a PartsTech link icon above Line 10 on your repair order screen. Click the icon and take a few minutes to explore this powerful new feature.

Everything You Need in One Place

Your Shop Management System is the hub of your business—tracking customers, repair history, labor, invoicing, and more. Now, with PartsTech built directly into the system, you no longer need to jump between multiple supplier websites or browser windows to find the right parts.

With a few clicks, you can:

- Search multiple parts suppliers at once.

- Compare pricing and availability.

- View real-time inventory and delivery estimates.

- Add selected parts directly to the active repair order.

The seamless integration eliminates unnecessary steps, saving valuable time while improving estimate accuracy and customer service.

Real-Time Information Means Better Productivity

Knowing which supplier has the part you need—and when it can be delivered—can make the difference between completing a repair today or delaying it until tomorrow.

PartsTech's cloud-based platform provides up-to-date inventory information and delivery estimates, allowing your shop to make informed purchasing decisions quickly. Faster ordering helps keep vehicles moving through the shop and technicians productive.

Take Advantage of This New Tool

If you haven't tried PartsTech yet, now is the perfect time. Simply click the PartsTech icon within your ASN Shop Management System and see how easy it is to search, compare, order, and add parts directly to your repair orders.

This is another example of ASN providing members with tools that improve efficiency, reduce wasted time, and help your shop operate more profitably.

Stay Ahead of Fraud

Posted Thursday, July 30, 2026

Fraud is constantly evolving, and criminals are becoming more sophisticated in the ways they target individuals and businesses. Staying informed and vigilant is one of the best ways to protect yourself and your finances.

This year, we're seeing a significant increase in several types of fraud, including:

- Phone Scams

- Business Email Compromise (BEC)

- Elder Financial Exploitation

- Online Ticket and Merchandise Scams

Beware of Phone Scams

One of the fastest-growing fraud tactics is caller ID spoofing, where scammers manipulate the caller ID to make it appear as though a call or text message is coming from your bank. Their goal is to create a sense of urgency and convince you to share sensitive personal or financial information.

Scammers often claim they have detected suspicious activity on your account and need to verify your identity. While a legitimate representative from your bank may contact you regarding account activity, they will never ask for:

- Your full debit card or account number

- Your online banking username or password

- Your one-time verification or multi-factor authentication (MFA) codes

If you receive a call or text that seems suspicious, hang up immediately and contact your bank using the phone number listed on its official website, the back of your debit card, or your account statement. A legitimate bank representative will always respect your decision to call the bank directly.

How You Can Protect Yourself

Protecting your accounts is a shared responsibility. These simple habits can significantly reduce your risk of becoming a victim of fraud:

- Stay cautious. Never share personal or financial information with someone who contacts you unexpectedly.

- Verify the caller's identity. If a call or text seems suspicious, hang up and contact your bank using a trusted phone number.

- Monitor your accounts regularly. Review your transactions frequently using your bank's mobile app or online banking and report any unauthorized activity immediately.

- Enable dual approval for wire and ACH transactions. Requiring a second approval helps verify transactions, reduces errors, and provides an additional layer of protection against fraud.

- Report concerns immediately. If you suspect fraud or notice unusual account activity, contact your bank as soon as possible.

Don't Let Scammers Ruin the Experience

With major sporting events, concerts, festivals, and other popular events taking place throughout the year, fraudsters are taking advantage of excited fans by creating fake websites and selling counterfeit tickets and merchandise.

Before making a purchase, remember these safety tips:

- Purchase tickets and merchandise only from official websites or authorized sellers.

- Verify the website address (URL) before entering payment information.

- Be cautious of unsolicited offers or prices that seem too good to be true.

- Never send payments using cryptocurrency, gift cards, or wire transfers when purchasing tickets or merchandise.

- Watch for warning signs such as spelling errors, poor website quality, or high-pressure tactics urging you to "buy now."

- Many legitimate websites ask you to verify you're human by selecting images. Be cautious if a website instead asks you to enter keyboard shortcuts, download software, or perform other unusual actions.

ASN Support Alert

Scammers frequently impersonate technology support providers and attempt to gain remote access to your computer.

Remember: ASN only uses ASN Tech Connect to establish a remote connection when you have contacted us and requested technical support. We will never make an unsolicited (cold) call asking to connect to your computer, and we do not use any remote access platform other than our own secure connection method.

If someone claiming to represent ASN contacts you unexpectedly and asks you to install software or grant remote access:

- Do not allow them to connect to your computer.

- Do not use any remote connection method suggested by the caller.

- Hang up immediately.

- Contact ASN directly using our published phone number to verify whether the request is legitimate.

When in doubt, always verify first. Taking a few extra moments to confirm who you're dealing with can help protect your personal information, your finances, and your peace of mind.

California sends Tesla a message with its new EV rebate

Posted Thursday, July 30, 2026

The statement is political, and Elon Musk won’t be happy.

Electric vehicles have had a rough year. Washington killed the $7,500 federal tax credit last September, and price-sensitive buyers scattered almost overnight. New EV sales fell 27% in the first quarter of 2026, sinking to 5.8% of the market, according to Cox Automotive.

California felt it worse than most. The state that built the American EV habit watched its own electric share slide toward levels it hadn’t seen in years, well short of the targets it set for itself.

So the state decided to step back in. Governor Gavin Newsom signed SB 168 on Monday, July 13, creating a program called MyFirstEV that takes $3,500 off an electric car right at the dealership. Read the fine print, though, and you find a rule that lifts Rivian and Lucid, caps Tesla (TSLA), and lands like a message addressed to Austin, Texas.

How the instant EV rebate works

MyFirstEV throws out the old model. California’s previous Clean Vehicle Rebate Project made buyers apply and wait for a check. This one is a point-of-sale discount, so eligible buyers walk into a participating dealership and drive out with the money already gone from the price.

The terms look simple on the surface.

- $3,500 off a new EV priced under $50,000, or $1,750 off a used one under $25,000, according to the Governor’s office.

- A combined pool near $270 million once automakers match the state’s $135.5 million, according to the Governor’s office.

- Rivian’s cheapest model runs about $58,000 and Lucid’s about $71,000, yet both still qualify, according to Electrek.

- New U.S. EV sales dropped 27% in the first quarter of 2026, according to Cox Automotive.

There is no income cap, which is the first thing that jumped out at me. California spent years making its incentives means-tested, steering the biggest help toward lower-income drivers. This program flips that.

Price is the only gate, the buyer has to be a California resident, and they just attest that this is their first zero-emission vehicle. A curb-weight limit of 8,500 pounds keeps it to ordinary passenger cars, and the California Air Resources Board (CARB) is still finalizing deals with automakers, with a launch expected later this summer.

The headquarters loophole that boxes out Tesla

Here is the part that turns a discount into a statement. That $50,000 price cap vanishes for EVs built by California-headquartered, EV-only automakers, judged by where a company’s management sat on January 1, 2026, according to Electrek. In practice, that describes exactly two carmakers.

Rivian (RIVN), with engineering offices in Irvine, makes the cut. So does Lucid (LCID), based in the San Francisco Bay Area. Their entry models sit thousands of dollars above the cap that binds everyone else, and they collect the full $3,500 anyway.

Tesla (TSLA) does not. The company moved its headquarters to Austin, Texas, in 2021, so it no longer counts as a California automaker under the rule. Only its sub-$50,000 Model 3 and Model Y configurations qualify. The Cybertruck, the Model S, and the Model X get nothing.

When I ran the eligible models against the price caps, the tell was obvious. The exemption rewards where a company keeps its logo, not where it builds its cars. Tesla still assembles hundreds of thousands of vehicles a year at its Fremont, California, plant, more EVs in the state than anyone. Rivian builds in Illinois. Lucid builds in Arizona.

The framing is hard to miss given the long public feud between Newsom and Tesla CEO Elon Musk. Newsom’s office cast the whole package as a stand against President Donald Trump’s push to “surrender the clean car industry to China on a silver platter,” according to the Governor’s office.

Electrek was blunter, writing that the carve-out “turns an affordability program into a political statement,” according to Electrek.

What the rebate means for California buyers

Strip away the politics, and the $3,500 is real money. For a family financing a new car, that is a few months of payments erased before they leave the lot, or a serious dent in the down payment on a tight budget.

The used-EV piece may matter even more. A wave of off-lease electric cars is landing on dealer lots, and $1,750 off a sub-$25,000 vehicle is the kind of discount a first-time buyer actually feels.

Plenty of mainstream options clear the $50,000 line. GM (GM) has the Equinox EV, the Blazer EV, and the Bolt, which starts under $30,000. Ford’s (F) Mustang Mach-E, Toyota’s bZ, and Hyundai’s Ioniq 5 all qualify too.

What struck me reading the bill was the quiet math of the no-income-cap rule. A first-time buyer picking up a $71,000 Lucid gets the same $3,500 as a family stretching for a $30,000 Bolt, and arguably a better deal, since that luxury sedan would not qualify for a dime anywhere else. A program sold as help for regular families also happens to underwrite some of the priciest EVs on the road.

Why this EV fight is far from over

The loophole is the kind of thing lawyers notice. Rewarding a corporate flag over actual California manufacturing invites a challenge, and Tesla, the state’s largest EV employer, would have a real argument that the rule punishes it for a headquarters address.

There is a bigger backdrop, too. The post-credit slump amounted to “a necessary reset,” according to Cox Automotive, and U.S. sales ticked back up in the second quarter as state programs stepped in, according to InsideEVs. California is betting it can rebuild that momentum one first-time buyer at a time.

The message to Tesla landed on July 13. The reply may come from a courtroom, and whatever a judge decides could tell every other state how far it can go in picking winners with public money.

Anyone shopping for a first EV this summer should read the sticker closely, because in California, the discount now depends on more than the car.

Source: TheSteet

Used-car market has ‘strength and resilience’ despite forecast of slightly softening sales

Posted Thursday, July 30, 2026

Cox Automotive recently projected slight softening of certified pre-owned vehicle sales and overall used-car retail transactions for the year.

But experts also see the movements reflected “strength and resilience” of the used-car market.

Let’s get into the numbers.

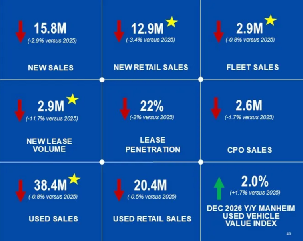

As part of its Q2 2026 Mid-Year Review in Detroit, Cox Automotive chief economist Jeremy Robb recapped that this year’s used-car retail sales are expected to come in at 38.4 million units, which would be down less than 1% year-over-year.

Robb added that Cox Automotive is still expecting to see 2.6 million CPO sales this year. That number would represent roughly a 2% drop compared to last year’s final tally.

The projections prompted Cox Automotive deputy chief economist Mark Strand to say, “When you combine the tough comp versus the tariff driven market frenzy with an energy shock, rising inflation and ongoing general affordability pressures, the small decline in the used sales pace looks like relative strength and resilience.”

As part of its Q2 2026 Mid-Year Review in Detroit, Cox Automotive chief economist Jeremy Robb recapped that this year’s used-car retail sales are expected to come in at 38.4 million units, which would be down less than 1% year-over-year.

Robb added that Cox Automotive is still expecting to see 2.6 million CPO sales this year. That number would represent roughly a 2% drop compared to last year’s final tally.

The projections prompted Cox Automotive deputy chief economist Mark Strand to say, “When you combine the tough comp versus the tariff driven market frenzy with an energy shock, rising inflation and ongoing general affordability pressures, the small decline in the used sales pace looks like relative strength and resilience.”

Source: AutoRemarketing

Car dealer closes 40% of its stores, shares bankruptcy warning

Posted Thursday, July 30, 2026

The company has warned that it may not have enough cash to survive.

I haven’t met many people who were actually able to afford a new car.

Sure, plenty buy them, but suffocating monthly loan payments mean the “affording” part isn’t exactly met.

For decades, we shrugged off the warning that a new car loses 10% of its value the second it leaves the lot. The counter-argument was simple: You paid for peace of mind and the guarantee you wouldn’t end up stranded on the road.

But today, even buying a used car is a crushing mathematical problem.

According to Edmunds, the average monthly new-car payment has hit a record $777, and 20.3% of buyers pay $1,000 or more monthly. To cope, many stretch loans over six or seven years. Edmunds’ Ivan Drury calls this a “mathematical trap,” warning that pairing a 7.0% APR with an 84-month loan means handing over nearly $10,000 in interest alone, leaving buyers “highly vulnerable to falling underwater.”

Used-car buyers are squeezed just as hard, financing an average of $30,414 at 10.5% interest. For subprime buyers, Experian data show interest rates averaging a staggering 19.4% to 21.7%.

That pressure isn’t just hurting buyers. It is also hitting the dealerships that specialize in financing customers with weaker credit. Now, one of the largest chains in the country has dramatically reduced its footprint.

A major automotive retailer that operates a chain of used-car dealerships, America’s Car-Mart reported on July 14, 2026, its fourth-quarter and full-year results for the period ended April 30, 2026.

The car dealer, which specializes in the “buy here, pay here” (integrated auto sales and financing) market, reported total revenue of $1.281 billion, down by 7.9% from fiscal 2025.

America’s Car-Mart full fiscal 2026 earnings vs. fiscal 2025:

- Gross profit per unit improved 1.0% to $7,442.

- Gross margin percentage of 35.4% versus 36.7%.

- Net loss amounted to $139.11 million, versus net income of $17.93 million.

- Net loss per share was $16.79, compared to earnings per share of $2.38.

In the report, America’s Car-Mart confirmed it has consolidated 60 dealership locations in the period of 12 months (from April 30, 2025, to April 30, 2026). The company’s active dealership count decreased from 154 to 94, resulting in a 40% footprint reduction.

Why has America’s Car-Mart been closing so many locations?

America’s Car-Mart began showing the first signs of trouble more than a year ago. After digging through its official reports, I found that in December 2025, the company’s official Q2 FY26 Management Script said it had closed a $300 million term loan that removed the capital-related limits to optimize its store footprint and organization structure.

“Now with more flexibility, we’re moving decisively on a multi-phase plan to optimize our footprint, cost structure, and strengthen capital efficiency,” stated America’s Car-Mart CEO Doug Campbell.

Campbell added that phase one was executed in early November by consolidating five underperforming stores and eliminating approximately 10% of its employees. The second phase was set for Q3 and was projected to result in more than $20 million in annualized SG&A savings.

On Jan. 13, America’s Car-Mart confirmed in a press release it has completed phase 2 by consolidating 13 of its locations into higher-performing nearby dealerships. Combined with phase 1, that makes 18 consolidated locations in those two phases.

As of the July 14 earnings release, the company has not yet disclosed the locations of the remaining 42 dealership locations that were consolidated in the fourth quarter of fiscal 2026.

“Faced with limited origination capital and no revolving warehouse facility, we intentionally reduced originations and inventory to protect liquidity and avoided originating loans we lack the capacity to carry,” Campbell said during the Q4 and full fiscal 2026 year earnings call.

America’s Car-Mart issues “going concern” disclosure

While retailers frequently close underperforming stores to improve profitability, the situation of America’s Car-Mart appears to go beyond routine cost-cutting.

As part of my recent retail tracking coverage for TheStreet, I’ve documented how several major mall staples are executing similar strategies to protect their profit margins. Fossil Group shuttered seven stores during the first quarter of 2026 alone, and Vera Bradley closed 13 underperforming retail locations.

Another example is fashion mall retailer Tilly’s, which successfully cut its rent and operating costs by closing 40 underperforming locations and opening 12 new ones over two years.

This optimization boosted quarterly gross profits to $36.1 million and dramatically shrank the company’s net losses. It recently confirmed plans to open three new stores later this year.

However, mall fashion retailers are a completely different type of business than a “buy here, pay here” car dealership, and the management views liquidity, not merely store efficiency, as the primary challenge.

In fact, Campbell confirmed in a call that there will be “going concern disclosure in our Form 10-K. It’s there because we have not secured additional financing or an alternative transaction that we need to resolve our liquidity constraint, not because anything changed in how our customers are paying us back.”

What is a “going concern”?

The going concern principle assumes that an organization or business is financially stable enough to continue to operate for the foreseeable future, typically the next 12 months.

A going concern disclosure does not mean a company will file for bankruptcy. It indicates that management has identified conditions that raise substantial doubt about the company’s ability to continue operating over the next year.

Source: TheStreet

What's New -July 2026

Posted Tuesday, June 30, 2026

Used-Car Market Shows Strength Despite Softer Outlook

Posted Tuesday, June 30, 2026

Focus on the Opening

Posted Tuesday, June 30, 2026

Car dealership warned about ‘deceptive pricing’ by the FTC

Posted Tuesday, June 30, 2026

VISALIA, Calif. A Visalia auto dealership was among almost 100 auto dealership groups nationwide warned by federal officials about advertising prices that customers could not actually receive.

The Federal Trade Commission (FTC) announced in March that it was sending letters to 97 auto dealership groups nationwide warning them that the prices they display must be the total price, including all mandatory fees.

Among the groups was Visalia Hyundai, located at 220 S. Ben Maddox Way in Visalia. A representative from Visalia Hyundai says they bought the dealership in January, and it’s now under new ownership.

The letter sent by the FTC to Visalia Hyundai alleges that the dealership was “advertising prices for cars that are lower than what you actually charge consumers.”

The FTC cites some of these “illegal pricing practices” as:

- Advertising a price that does not reflect all required fees

- Advertising a price that reflects rebates or discounts not available to all consumers

- Advertising a price that fails to take into account the amount of an additional required down payment

- Conditioning the advertised price on consumers using dealer financing

- Requiring consumers to buy additional items not reflected in the advertised price

- Advertising unavailable or nonexistent vehicles

The FTC stated they reached out to Visalia Hyundai because they were “concerned” the dealership “may be engaging in one or more of these practices.”

The representative of the dealership said that the new ownership had nothing to do with the deceptive pricing allegations.

“This letter is not intended to be a comprehensive statement of concerns that may exist about your dealership or dealership group. Nor is it intended to represent any conclusions on whether your dealership or dealership group is engaging in these practices,” the letter read in part.

The FTC stated that the warnings issued are part of a wider effort to examine all markets, including rental housing, grocery delivery services, and hotels.

Source: CBS47

Pandemic Supply Gaps Continue to Impact Vehicle Prices

Posted Tuesday, June 30, 2026

- Pandemic-era vehicle shortages are still affecting used car prices.

- The auto industry is producing fewer cars than it used to, which means high new vehicle prices and other costs are pushing more consumers into the used market while supply is tight.

- Lower new car volumes could be a new normal, constricting supply for years to come.

The shockwaves of the Covid-19 pandemic are still hitting the U.S. car market and pushing prices up, even for exceptionally old cars.

The pandemic dealt a severe blow to the total supply of new cars, which has rippled down to the used market.

About 8 million vehicles that would have been made for U.S. buyers during those years never were, largely due to production shutdowns and supply shortages, said Jeremy Robb, chief economist for Cox Automotive. Automakers faced with curtailed production weighted their lineups toward money-making high-end vehicles, a strategy they have largely continued.

These factors have been pushing up prices for everyone — even customers buying decade-old used vehicles.

“I think it’s kind of the new normal outside of a big economic impact,” Robb said. “Supply is not getting a lot better over the next three to four years.”

About 16.2 million cars were sold in 2025, up from the pandemic-era low of 13.8 million in 2022, according to the U.S. Bureau of Economic Analysis. Cox is forecasting about 15.8 million vehicles will be sold in 2026, while JD Power is predicting 16.3 million.

That’s a significant drop from the record 17.55 million vehicles sold in 2016.

Volumes were already dropping before the pandemic set in. The auto market is historically cyclical, so sales go up and down.

But JD Power Senior Vice President Tyson Jominy said the U.S. auto industry has sold roughly 16 million fewer vehicles than it would have if annual sales had held at the 2016 record of 17.5 million. That is about a year’s worth of volume gone — about half of it since the pandemic.

Fewer vehicles coming to the new market have constrained supply in the used one.

“A new vehicle sale is the marble at the top of the mousetrap game,” Jominy said. “And when you drop that marble, it’s going to go through all the chutes and ladders all the way down to the bottom.”

Leasing and incentives

In addition to tighter supply, automakers and dealers have also cut back on industry practices like leasing and incentives because supply was so short.

“Leasing is really expensive for an OEM,” Robb said, referring to the acronym that stands for original equipment manufacturer, another name for automakers.

Typically, payments are lower for leases, there can be lots of upfront costs for the manufacturer and when the car comes back it has to be flipped into the used market, among other things, he said.

“The OEMs really leaned into building more profitable cars like trim levels, trucks, SUVs, things like that,” Robb said. “And those, they’re more expensive. They tend not to get leased as much.”

Off-lease vehicles are a big pipeline for the used market. Prior to the pandemic, leasing was roughly 30% of the new vehicle market, Robb said. In 2022, it hit a low of 18%.

Because most leases are for three years, it has taken that long for the used market to feel the wave.

Automakers also don’t want to have to discount vehicles if they don’t have to. During the pandemic, they didn’t need to.

Incentives — essentially discounts on new cars — averaged about 9.5% of vehicle prices across the new car market before the pandemic, according to Cox Automotive. During the pandemic, they fell to a fraction of that. They’ve climbed back up, averaging about 6.5% to 7% in 2026, Cox’s Robb said. But that is still low compared with prepandemic levels, and they aren’t represented evenly across the industry.

All this means that used car prices have stayed relatively high.

Meanwhile, consumers are facing high gas prices, inflation and increased expenses across the board.

“Prices have gone up about a third and yet salaries and income have not nearly matched those increases,” JD Power’s Jominy said. “There’s a smaller group of buyers that can afford new vehicles. The average new vehicle household income is over $150,000 a year versus about $80,000 for the U.S. economy as a whole.”

Data from Cox Automotive shows that demand for even 9- and 10-year-old used vehicles is much higher than it has historically been. That indicates that more consumers are trading down and seeking out ever-older and cheaper cars as prices rise.

“We don’t normally see this kind of pricing pressure in the lower end of the market,” Robb said.

Source: CNBC

What's New -June 2026

Posted Monday, June 1, 2026

Sales

-

New Feature: Enhanced Vehicle Sales Quote for FTC Compliance

We've completely redesigned the Vehicle Sales Quote in the Sales tab to better align with new FTC disclosure requirements and improve the customer experience.

The updated quote provides clearer itemization of:

- Vehicle accessories

- Optional products and protections

- Product pricing and disclosures

In addition, the quote now includes enhanced language clarifying that aftermarket products, service contracts, GAP, and other optional products are voluntary and not required for vehicle purchase or financing approval.

Beyond compliance improvements, the entire quote layout has been reorganized to present information in a more professional, efficient, and easy-to-understand format for both your staff and customers.

You also have the option to add your dealership logo to the quote using the "Pmt Option" feature and a logo image link, helping create a more branded and professional presentation for your customers.

Contracts

-

New Form Added: Rhode Island DMV Form T-334

The Rhode Island DMV Form T-334 (Sales Tax Form) has been added to the Contract tab.

Dealers can now easily access and print this form directly from the sales process, helping streamline Rhode Island transactions and ensure the required sales tax documentation is included with the deal paperwork.

This enhancement simplifies compliance and reduces the need to manage the form outside the system.

-

Update: California DMV Form 227

California dealers now have access to the updated DMV Form 227 within the system.

This update ensures dealers are working with the latest required DMV documentation for title and registration-related processes.

The form is now available for use.

Inventory

-

New Audit Log: Stock Number Creation Tracking

A new audit log has been added to track who originally created a stock number, even when no changes have been made to the record.

This enhancement gives management greater visibility into the initial data entry process. If a stock record contains incorrect or incomplete information, your team can quickly identify who entered the original record and provide additional training or guidance as needed.

This feature helps improve accountability, data accuracy, and inventory management procedures throughout the dealership.

Bookkeeping

-

Update: Sales Tax Due Date Alignment

We've made an enhancement to Sales Tax processing so that the sales tax due date will now automatically match the vehicle sale date.

This change helps ensure greater consistency between the transaction date and the related tax records, improving reporting accuracy and simplifying sales tax tracking and reconciliation.

This update is designed to reduce confusion and provide a more streamlined accounting workflow.

Update: Collection Tab – ASN AI Collector Agent

The ASN AI Collector Agent in the Collection tab continues to improve efficiency in communicating with past-due customers to help resolve account status, secure payments, or establish acceptable promises to pay.

The AI agent can send payment requests, encourage resolution, and assist customers in setting up recurring payments, along with other available payment options in real time.

It also helps ensure follow-up continuity by engaging with customers who respond via text when the collections team has not yet replied.

Contact our office to learn more about how to improve collection efficiency using the ASN AI Collector Agent.

Shop

-

New Feature Availability: Parts Markup Matrix for Service Shops

Service shop users now have the ability to apply in-house parts markup using a price matrix, instead of a single flat percentage across all parts.

This enhancement aligns in-house parts pricing with the existing retail parts matrix, allowing markup rules to vary based on part cost ranges. The result is more consistent pricing logic and improved control over service department profitability.

This feature is now available for configuration.

Software Tip: ASN Menu Financing Behavior Clarification

When using ASN Menu, please note the following behavior update:

If accessories are included as part of the base payment structure, the amount financed will always include those accessories. Financing calculations are configured accordingly to ensure all included items are properly reflected in the total financed amount.

Latest System Update

-

The Upcoming version is 7.0.19.21 —Our newest update is rolling out in phases. If you don’t see it yet, no action is needed; it will arrive automatically. Once updated, you’ll have access to the latest features and improvements to keep your system running at its best.

The Next Loyalty Windfall for Dealers? Gen Z

Posted Monday, June 1, 2026

Gen Z may be early in their ownership journey, but the service experiences they have today are already shaping where they’ll return tomorrow—both for service and their next vehicle. As this generation moves more fully into ownership, expectations set outside the automotive industry are colliding with long-standing dealership processes. The result is a defining moment for dealers: one that can either erode trust or build loyalty that lasts for decades.

Today, Gen Z still turns to dealerships for service. But there are early signs that traditional models aren’t fully keeping pace. Recent research shows that satisfaction is softening, even as loyalty largely holds, and alternative service options like mobile service are gaining attention. Those shifts point to a growing disconnect between what younger customers expect and what the traditional service experience often delivers.

That disconnect often appears before a customer ever sets foot in the dealership. Even as demand for digital engagement grows, scheduling service can still feel harder than it should. Phone calls, long wait times, and unclear systems add friction early in the process. For Gen Z—accustomed to instant, on-demand access across nearly every part of life—friction at the scheduling stage isn’t just inconvenient; it’s a reason to disengage altogether.

Where Expectations Are Won—or Lost

With average transaction prices reaching roughly $35,000 for cars and exceeding $50,000 for trucks, service decisions no longer feel low-stakes—especially for younger buyers. Every interaction reinforces whether that investment feels protected or at risk, raising expectations for clarity, consistency, and trust across the service experience.

Digital access plays a key role in shaping those perceptions. It’s not just about convenience; it’s how customers judge competence. For Gen Z, intuitive online tools signal that a dealership is organized, transparent, and respectful of their time. When self-service options are hard to find—or missing entirely—dealerships risk being ruled out before a relationship even begins.

Recall appointments create another critical moment. They remain a dependable reason customers return to dealerships, but for Gen Z, these visits carry added weight. Younger customers are often open to additional services during recall visits, yet they’re also quick to delay or opt out if timing, pricing, or next steps feel unclear. Clear communication at this stage can strengthen trust—or quietly undermine it.

As ownership cycles stretch and budgets tighten, predictability has become just as important as speed. Many customers are focused on keeping vehicles longer, and satisfaction rises when service stays aligned with expectations—even if repairs take extra time. Across generations, delivering on what was promised matters more than moving fast. For Gen Z, changes without explanation are especially costly to trust.

Gen Z is Still Coming to the Dealership

Despite their digital-first reputation, Gen Z hasn’t abandoned the physical dealership. Industry data shows that over 50% of customers choose to wait onsite during service—but expectations have changed. Comfortable seating, reliable connectivity, and spaces that support productivity now signal professionalism and respect for customers’ time.

Gen Z loyalty starts early, with the majority getting their vehicles serviced at the same dealership where they bought them. That makes early service experiences decisive moments, shaping trust and influencing future purchase decisions. The service lane isn’t just about today’s visit—it’s the gateway to long-term loyalty. Dealers that remove friction, communicate clearly, and follow through on their promises can earn Gen Z customers not just once, but for a lifetime.

Feds Withdraw Statement on Immigration Status of Noncitizen Borrowers

Posted Monday, June 1, 2026

Washington, D.C. – The Consumer Financial Protection Bureau and the Department of Justice announced that they have withdrawn a joint statement regarding the implications of a creditor’s consideration of an individual’s immigration status under the Equal Credit Opportunity Act (ECOA).

On October 12, 2023, the agencies published a joint statement cautioning that creditor policies related to an applicant’s immigration or citizenship status could, in certain circumstances, run afoul of ECOA’s and Regulation B’s prohibition of discrimination on the basis of protected classes, including race and national origin. The agencies withdrew the joint statement to avoid any conflict with the express language of ECOA and its implementing regulation, Regulation B.

“For decades, ECOA regulations have permitted lenders to consider a borrower’s lawful residence status and other information necessary to protect their rights and remedies with respect to repayment,” said Acting Director Russell Vought at the Consumer Financial Protection Bureau. “We are correcting the last administration’s attempt to ignore these well-accepted and common-sense principles of our nation’s fair lending laws.”

“The federal government is committed to avoiding statements that could confuse the law or imply compliance standards for civil rights laws that lack any statutory or regulatory basis,” said Assistant Attorney General Harmeet K. Dhillon at the Justice Department’s Civil Rights Division. “This administration is restoring alignment with established federal civil rights law rather than continuing the prior administration’s ideologically-driven departures.”

ECOA and Regulation B respectively permit creditors to consider pertinent elements of credit-worthiness and information necessary to protect creditor rights and remedies, including a borrower’s immigration or citizenship status. The agencies also believe withdrawal is appropriate to avoid any confusion that lenders may legitimately consider immigration status under several circumstances, including when necessary to avoid financial risks and to comply with other laws. In addition, withdrawal is appropriate to address any misimpression that the joint statement interprets 42 U.S.C. § 1981 to confer any liability under the statute that has not already been recognized by courts. Finally, the agencies believe withdrawal is appropriate to avoid any unnecessary burdens from new or increased compliance efforts.

Catalyst IQ & JD Power explain underlying reasons why retail prices for used cars keep rising

Posted Monday, June 1, 2026

Catalyst IQ and JD Power each offered some clarity for why used-car retail prices are climbing even faster than ones for new models, which are just $30 below the record level seen in July 2023.

And perhaps more importantly for dealerships, Catalyst IQ also provided six recommendations to help stores navigate affordability pressures potential buyers are facing.

According to exclusive information shared with Cherokee Media Group on Friday, Catalyst IQ new-vehicle prices have climbed almost $1,000, or 1.9%, year-over-year, while vehicle movement per day has dropped by almost 5%.

Used-vehicle prices, meanwhile, have jumped even more at 6.1%, with vehicle movement down by just 1.0%, according to Catalyst IQ.

“We’re seeing a significant affordability impact on the used-car market with used vehicle prices increasing 6.1% year-over-year compared with 1.9% for new vehicles,” said Rick Wainschel, vice president of data science and analytics at Catalyst IQ.

“As we saw earlier this week in the (Wall Street Journal), consumers are still moving into used inventory, but affordability pressures are impacting all aspects of this market,” Wainschel continued in the message to Cherokee Media Group.

“While the data doesn’t point to a specific price threshold, it does show that as new vehicle prices move above $50,000, many consumers continue searching for lower-cost alternatives. It’s also important to understand that used vehicle movement has declined far less than new vehicle movement (1.0% vs. 4.7%), suggesting consumers still view used inventory as a relative value alternative even as prices rise across all sectors,” Wainschel went on to say.

So, that analysis likely prompts this question. How did we get here?

Well, following the publishing of that article by the Wall Street Journal that Wainschel mentioned, JD Power’s Tyson Jominy added more context to the company data cited by the newspaper.

Jominy, who is senior vice president of data and analytics at JD Power, pushed back on the thinking that new-car sales suddenly fell off the table, creating an unexpected dearth in the used-vehicle market. Rather, Jominy explained in this LinkedIn post that the deterioration of new-car sales has been happening for a decade that’s compounding the price and affordability situations.

“Industry total sales peaked in 2016 (2015 for retail sales), which means we are over a decade removed from peak vehicle sales in the U.S.,” Jominy wrote. “We aren’t just losing a million sales this year; we have been losing sales every year for a decade.

“We lost 3 million during COVID alone, then another 3.7 million during the supply chain crisis,” he continued. “Cumulative sales losses are 16.1 million over the past decade, nearly matching our forecast for the year.

“In short, the industry has lost an entire year’s worth of new-vehicle sales over this past decade,” Jominy went on to state.

And perhaps in a twist, as those sales are declined, prices have rocketed higher.

Catalyst IQ data shows average marketed price (AMP) is approaching an all-time high, reaching $51,610 on May 26, just

Over the past year, AMP increased by $1,896 with almost 85% of that growth taking place since March 1 alone. Coupled with affordability pressures, higher interest rates, and fuel prices approaching all-time highs—up more than $1.50 per gallon over the past eleven weeks—this rapid price growth is creating additional challenges for dealers entering the summer selling season.

“Historically, rising new-vehicle prices have created tailwinds for used demand as affordability-conscious consumers shifted into pre-owned inventory. That dynamic still appears to be playing out today, but with important limitations,” Wainschel told Cherokee Media Group.

Through a separate news release, Wainschel gave more insight through the prism of new models.

“Historically, higher vehicle prices were often temporary and corrected quickly through incentives or discounting,” Wainschel said. “This shift is fundamentally different for the industry. Several of the most profitable vehicle categories — including full-size trucks, full-size SUVs, heavy-duty trucks, and luxury midsize SUVs — are reaching all-time highs. These MSRP-driven price increases are resetting long-term pricing levels, making them more difficult to reverse.”

Catalyst IQ then explained this environment creates both opportunity and risk as consumer shopping behavior is influenced unevenly across segments, geographies, and vehicle configurations.

“It comes down to understanding where demand remains resilient and looking for pockets where affordability resistance is emerging,” Wainschel said. “Dealers who understand that every segment, trim and brand behaves differently in this market will be the ones who are successful in keeping business steady and earning customers’ business as they navigate current economic conditions.”

Easier said than done, right? Well, Catalyst IQ offered a few recommendations in a blog post that accompanied its data.

Here are six strategies Catalyst IQ suggested for dealerships operating in this higher-priced market.

- Audit price position, then act surgically

“As pricing rises, not every VIN requires the same strategy. Use VIN-level market intelligence to identify which vehicles remain competitively positioned and which are beginning to face price resistance. Protect margin where demand supports it, while making targeted adjustments only where needed.”

- Use lower-priced new, used, and certified inventory as affordability release valves

“As vehicle prices climb, a focus on more affordable models and trims informs consumers that there are still accessible choices to consider (see list below*). Additionally, used and certified inventory can become increasingly important alternatives for payment-sensitive shoppers. Dealers that strategically position vehicles that are within the means of a larger proportion of consumers can be better positioned to preserve volume and retain consumers who are stretching on affordability.”

- Protect volume by strengthening top-of-funnel visibility

“In higher-priced segments, shoppers often take longer to make decisions and compare more options before converting. Maintaining strong upper-funnel visibility helps ensure your dealership stays in the consideration set without relying too heavily on broad discounting.”

- Rebuild the message around total value, not just sticker price

“As affordability pressure increases, consumers look beyond monthly payments alone. Reinforce ownership value, capability, warranty coverage, fuel efficiency, and real-world usefulness consistently across digital advertising and vehicle detail pages.”

- Expand reach selectively based on demand signals

“Broader geographic or platform expansion can create opportunity, but only when supported by data. Use localized demand and inventory insights to identify where incremental reach is most likely to drive efficient results.”

- Monitor market resistance and adjust quickly

“In a fast-moving pricing environment, conditions can shift rapidly by segment, geography, and even individual configurations. Dealers that regularly evaluate pricing position, demand signals, and inventory efficiency will be better positioned to respond before resistance turns into aging inventory and wasted spend.”