What's New -July 2026

Posted Tuesday, June 30, 2026

Used-Car Market Shows Strength Despite Softer Outlook

Posted Tuesday, June 30, 2026

Focus on the Opening

Posted Tuesday, June 30, 2026

Car dealership warned about ‘deceptive pricing’ by the FTC

Posted Tuesday, June 30, 2026

VISALIA, Calif. A Visalia auto dealership was among almost 100 auto dealership groups nationwide warned by federal officials about advertising prices that customers could not actually receive.

The Federal Trade Commission (FTC) announced in March that it was sending letters to 97 auto dealership groups nationwide warning them that the prices they display must be the total price, including all mandatory fees.

Among the groups was Visalia Hyundai, located at 220 S. Ben Maddox Way in Visalia. A representative from Visalia Hyundai says they bought the dealership in January, and it’s now under new ownership.

The letter sent by the FTC to Visalia Hyundai alleges that the dealership was “advertising prices for cars that are lower than what you actually charge consumers.”

The FTC cites some of these “illegal pricing practices” as:

- Advertising a price that does not reflect all required fees

- Advertising a price that reflects rebates or discounts not available to all consumers

- Advertising a price that fails to take into account the amount of an additional required down payment

- Conditioning the advertised price on consumers using dealer financing

- Requiring consumers to buy additional items not reflected in the advertised price

- Advertising unavailable or nonexistent vehicles

The FTC stated they reached out to Visalia Hyundai because they were “concerned” the dealership “may be engaging in one or more of these practices.”

The representative of the dealership said that the new ownership had nothing to do with the deceptive pricing allegations.

“This letter is not intended to be a comprehensive statement of concerns that may exist about your dealership or dealership group. Nor is it intended to represent any conclusions on whether your dealership or dealership group is engaging in these practices,” the letter read in part.

The FTC stated that the warnings issued are part of a wider effort to examine all markets, including rental housing, grocery delivery services, and hotels.

Source: CBS47

Pandemic Supply Gaps Continue to Impact Vehicle Prices

Posted Tuesday, June 30, 2026

- Pandemic-era vehicle shortages are still affecting used car prices.

- The auto industry is producing fewer cars than it used to, which means high new vehicle prices and other costs are pushing more consumers into the used market while supply is tight.

- Lower new car volumes could be a new normal, constricting supply for years to come.

The shockwaves of the Covid-19 pandemic are still hitting the U.S. car market and pushing prices up, even for exceptionally old cars.

The pandemic dealt a severe blow to the total supply of new cars, which has rippled down to the used market.

About 8 million vehicles that would have been made for U.S. buyers during those years never were, largely due to production shutdowns and supply shortages, said Jeremy Robb, chief economist for Cox Automotive. Automakers faced with curtailed production weighted their lineups toward money-making high-end vehicles, a strategy they have largely continued.

These factors have been pushing up prices for everyone — even customers buying decade-old used vehicles.

“I think it’s kind of the new normal outside of a big economic impact,” Robb said. “Supply is not getting a lot better over the next three to four years.”

About 16.2 million cars were sold in 2025, up from the pandemic-era low of 13.8 million in 2022, according to the U.S. Bureau of Economic Analysis. Cox is forecasting about 15.8 million vehicles will be sold in 2026, while JD Power is predicting 16.3 million.

That’s a significant drop from the record 17.55 million vehicles sold in 2016.

Volumes were already dropping before the pandemic set in. The auto market is historically cyclical, so sales go up and down.

But JD Power Senior Vice President Tyson Jominy said the U.S. auto industry has sold roughly 16 million fewer vehicles than it would have if annual sales had held at the 2016 record of 17.5 million. That is about a year’s worth of volume gone — about half of it since the pandemic.

Fewer vehicles coming to the new market have constrained supply in the used one.

“A new vehicle sale is the marble at the top of the mousetrap game,” Jominy said. “And when you drop that marble, it’s going to go through all the chutes and ladders all the way down to the bottom.”

Leasing and incentives

In addition to tighter supply, automakers and dealers have also cut back on industry practices like leasing and incentives because supply was so short.

“Leasing is really expensive for an OEM,” Robb said, referring to the acronym that stands for original equipment manufacturer, another name for automakers.

Typically, payments are lower for leases, there can be lots of upfront costs for the manufacturer and when the car comes back it has to be flipped into the used market, among other things, he said.

“The OEMs really leaned into building more profitable cars like trim levels, trucks, SUVs, things like that,” Robb said. “And those, they’re more expensive. They tend not to get leased as much.”

Off-lease vehicles are a big pipeline for the used market. Prior to the pandemic, leasing was roughly 30% of the new vehicle market, Robb said. In 2022, it hit a low of 18%.

Because most leases are for three years, it has taken that long for the used market to feel the wave.

Automakers also don’t want to have to discount vehicles if they don’t have to. During the pandemic, they didn’t need to.

Incentives — essentially discounts on new cars — averaged about 9.5% of vehicle prices across the new car market before the pandemic, according to Cox Automotive. During the pandemic, they fell to a fraction of that. They’ve climbed back up, averaging about 6.5% to 7% in 2026, Cox’s Robb said. But that is still low compared with prepandemic levels, and they aren’t represented evenly across the industry.

All this means that used car prices have stayed relatively high.

Meanwhile, consumers are facing high gas prices, inflation and increased expenses across the board.

“Prices have gone up about a third and yet salaries and income have not nearly matched those increases,” JD Power’s Jominy said. “There’s a smaller group of buyers that can afford new vehicles. The average new vehicle household income is over $150,000 a year versus about $80,000 for the U.S. economy as a whole.”

Data from Cox Automotive shows that demand for even 9- and 10-year-old used vehicles is much higher than it has historically been. That indicates that more consumers are trading down and seeking out ever-older and cheaper cars as prices rise.

“We don’t normally see this kind of pricing pressure in the lower end of the market,” Robb said.

Source: CNBC

What's New -June 2026

Posted Monday, June 1, 2026

Sales

-

New Feature: Enhanced Vehicle Sales Quote for FTC Compliance

We've completely redesigned the Vehicle Sales Quote in the Sales tab to better align with new FTC disclosure requirements and improve the customer experience.

The updated quote provides clearer itemization of:

- Vehicle accessories

- Optional products and protections

- Product pricing and disclosures

In addition, the quote now includes enhanced language clarifying that aftermarket products, service contracts, GAP, and other optional products are voluntary and not required for vehicle purchase or financing approval.

Beyond compliance improvements, the entire quote layout has been reorganized to present information in a more professional, efficient, and easy-to-understand format for both your staff and customers.

You also have the option to add your dealership logo to the quote using the "Pmt Option" feature and a logo image link, helping create a more branded and professional presentation for your customers.

Contracts

-

New Form Added: Rhode Island DMV Form T-334

The Rhode Island DMV Form T-334 (Sales Tax Form) has been added to the Contract tab.

Dealers can now easily access and print this form directly from the sales process, helping streamline Rhode Island transactions and ensure the required sales tax documentation is included with the deal paperwork.

This enhancement simplifies compliance and reduces the need to manage the form outside the system.

-

Update: California DMV Form 227

California dealers now have access to the updated DMV Form 227 within the system.

This update ensures dealers are working with the latest required DMV documentation for title and registration-related processes.

The form is now available for use.

Inventory

-

New Audit Log: Stock Number Creation Tracking

A new audit log has been added to track who originally created a stock number, even when no changes have been made to the record.

This enhancement gives management greater visibility into the initial data entry process. If a stock record contains incorrect or incomplete information, your team can quickly identify who entered the original record and provide additional training or guidance as needed.

This feature helps improve accountability, data accuracy, and inventory management procedures throughout the dealership.

Bookkeeping

-

Update: Sales Tax Due Date Alignment

We've made an enhancement to Sales Tax processing so that the sales tax due date will now automatically match the vehicle sale date.

This change helps ensure greater consistency between the transaction date and the related tax records, improving reporting accuracy and simplifying sales tax tracking and reconciliation.

This update is designed to reduce confusion and provide a more streamlined accounting workflow.

Update: Collection Tab – ASN AI Collector Agent

The ASN AI Collector Agent in the Collection tab continues to improve efficiency in communicating with past-due customers to help resolve account status, secure payments, or establish acceptable promises to pay.

The AI agent can send payment requests, encourage resolution, and assist customers in setting up recurring payments, along with other available payment options in real time.

It also helps ensure follow-up continuity by engaging with customers who respond via text when the collections team has not yet replied.

Contact our office to learn more about how to improve collection efficiency using the ASN AI Collector Agent.

Shop

-

New Feature Availability: Parts Markup Matrix for Service Shops

Service shop users now have the ability to apply in-house parts markup using a price matrix, instead of a single flat percentage across all parts.

This enhancement aligns in-house parts pricing with the existing retail parts matrix, allowing markup rules to vary based on part cost ranges. The result is more consistent pricing logic and improved control over service department profitability.

This feature is now available for configuration.

Software Tip: ASN Menu Financing Behavior Clarification

When using ASN Menu, please note the following behavior update:

If accessories are included as part of the base payment structure, the amount financed will always include those accessories. Financing calculations are configured accordingly to ensure all included items are properly reflected in the total financed amount.

Latest System Update

-

The Upcoming version is 7.0.19.21 —Our newest update is rolling out in phases. If you don’t see it yet, no action is needed; it will arrive automatically. Once updated, you’ll have access to the latest features and improvements to keep your system running at its best.

The Next Loyalty Windfall for Dealers? Gen Z

Posted Monday, June 1, 2026

Gen Z may be early in their ownership journey, but the service experiences they have today are already shaping where they’ll return tomorrow—both for service and their next vehicle. As this generation moves more fully into ownership, expectations set outside the automotive industry are colliding with long-standing dealership processes. The result is a defining moment for dealers: one that can either erode trust or build loyalty that lasts for decades.

Today, Gen Z still turns to dealerships for service. But there are early signs that traditional models aren’t fully keeping pace. Recent research shows that satisfaction is softening, even as loyalty largely holds, and alternative service options like mobile service are gaining attention. Those shifts point to a growing disconnect between what younger customers expect and what the traditional service experience often delivers.

That disconnect often appears before a customer ever sets foot in the dealership. Even as demand for digital engagement grows, scheduling service can still feel harder than it should. Phone calls, long wait times, and unclear systems add friction early in the process. For Gen Z—accustomed to instant, on-demand access across nearly every part of life—friction at the scheduling stage isn’t just inconvenient; it’s a reason to disengage altogether.

Where Expectations Are Won—or Lost

With average transaction prices reaching roughly $35,000 for cars and exceeding $50,000 for trucks, service decisions no longer feel low-stakes—especially for younger buyers. Every interaction reinforces whether that investment feels protected or at risk, raising expectations for clarity, consistency, and trust across the service experience.

Digital access plays a key role in shaping those perceptions. It’s not just about convenience; it’s how customers judge competence. For Gen Z, intuitive online tools signal that a dealership is organized, transparent, and respectful of their time. When self-service options are hard to find—or missing entirely—dealerships risk being ruled out before a relationship even begins.

Recall appointments create another critical moment. They remain a dependable reason customers return to dealerships, but for Gen Z, these visits carry added weight. Younger customers are often open to additional services during recall visits, yet they’re also quick to delay or opt out if timing, pricing, or next steps feel unclear. Clear communication at this stage can strengthen trust—or quietly undermine it.

As ownership cycles stretch and budgets tighten, predictability has become just as important as speed. Many customers are focused on keeping vehicles longer, and satisfaction rises when service stays aligned with expectations—even if repairs take extra time. Across generations, delivering on what was promised matters more than moving fast. For Gen Z, changes without explanation are especially costly to trust.

Gen Z is Still Coming to the Dealership

Despite their digital-first reputation, Gen Z hasn’t abandoned the physical dealership. Industry data shows that over 50% of customers choose to wait onsite during service—but expectations have changed. Comfortable seating, reliable connectivity, and spaces that support productivity now signal professionalism and respect for customers’ time.

Gen Z loyalty starts early, with the majority getting their vehicles serviced at the same dealership where they bought them. That makes early service experiences decisive moments, shaping trust and influencing future purchase decisions. The service lane isn’t just about today’s visit—it’s the gateway to long-term loyalty. Dealers that remove friction, communicate clearly, and follow through on their promises can earn Gen Z customers not just once, but for a lifetime.

Feds Withdraw Statement on Immigration Status of Noncitizen Borrowers

Posted Monday, June 1, 2026

Washington, D.C. – The Consumer Financial Protection Bureau and the Department of Justice announced that they have withdrawn a joint statement regarding the implications of a creditor’s consideration of an individual’s immigration status under the Equal Credit Opportunity Act (ECOA).

On October 12, 2023, the agencies published a joint statement cautioning that creditor policies related to an applicant’s immigration or citizenship status could, in certain circumstances, run afoul of ECOA’s and Regulation B’s prohibition of discrimination on the basis of protected classes, including race and national origin. The agencies withdrew the joint statement to avoid any conflict with the express language of ECOA and its implementing regulation, Regulation B.

“For decades, ECOA regulations have permitted lenders to consider a borrower’s lawful residence status and other information necessary to protect their rights and remedies with respect to repayment,” said Acting Director Russell Vought at the Consumer Financial Protection Bureau. “We are correcting the last administration’s attempt to ignore these well-accepted and common-sense principles of our nation’s fair lending laws.”

“The federal government is committed to avoiding statements that could confuse the law or imply compliance standards for civil rights laws that lack any statutory or regulatory basis,” said Assistant Attorney General Harmeet K. Dhillon at the Justice Department’s Civil Rights Division. “This administration is restoring alignment with established federal civil rights law rather than continuing the prior administration’s ideologically-driven departures.”

ECOA and Regulation B respectively permit creditors to consider pertinent elements of credit-worthiness and information necessary to protect creditor rights and remedies, including a borrower’s immigration or citizenship status. The agencies also believe withdrawal is appropriate to avoid any confusion that lenders may legitimately consider immigration status under several circumstances, including when necessary to avoid financial risks and to comply with other laws. In addition, withdrawal is appropriate to address any misimpression that the joint statement interprets 42 U.S.C. § 1981 to confer any liability under the statute that has not already been recognized by courts. Finally, the agencies believe withdrawal is appropriate to avoid any unnecessary burdens from new or increased compliance efforts.

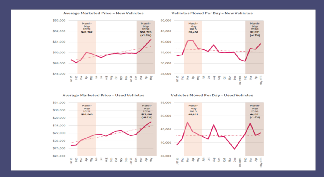

Catalyst IQ & JD Power explain underlying reasons why retail prices for used cars keep rising

Posted Monday, June 1, 2026

Catalyst IQ and JD Power each offered some clarity for why used-car retail prices are climbing even faster than ones for new models, which are just $30 below the record level seen in July 2023.

And perhaps more importantly for dealerships, Catalyst IQ also provided six recommendations to help stores navigate affordability pressures potential buyers are facing.

According to exclusive information shared with Cherokee Media Group on Friday, Catalyst IQ new-vehicle prices have climbed almost $1,000, or 1.9%, year-over-year, while vehicle movement per day has dropped by almost 5%.

Used-vehicle prices, meanwhile, have jumped even more at 6.1%, with vehicle movement down by just 1.0%, according to Catalyst IQ.

“We’re seeing a significant affordability impact on the used-car market with used vehicle prices increasing 6.1% year-over-year compared with 1.9% for new vehicles,” said Rick Wainschel, vice president of data science and analytics at Catalyst IQ.

“As we saw earlier this week in the (Wall Street Journal), consumers are still moving into used inventory, but affordability pressures are impacting all aspects of this market,” Wainschel continued in the message to Cherokee Media Group.

“While the data doesn’t point to a specific price threshold, it does show that as new vehicle prices move above $50,000, many consumers continue searching for lower-cost alternatives. It’s also important to understand that used vehicle movement has declined far less than new vehicle movement (1.0% vs. 4.7%), suggesting consumers still view used inventory as a relative value alternative even as prices rise across all sectors,” Wainschel went on to say.

So, that analysis likely prompts this question. How did we get here?

Well, following the publishing of that article by the Wall Street Journal that Wainschel mentioned, JD Power’s Tyson Jominy added more context to the company data cited by the newspaper.

Jominy, who is senior vice president of data and analytics at JD Power, pushed back on the thinking that new-car sales suddenly fell off the table, creating an unexpected dearth in the used-vehicle market. Rather, Jominy explained in this LinkedIn post that the deterioration of new-car sales has been happening for a decade that’s compounding the price and affordability situations.

“Industry total sales peaked in 2016 (2015 for retail sales), which means we are over a decade removed from peak vehicle sales in the U.S.,” Jominy wrote. “We aren’t just losing a million sales this year; we have been losing sales every year for a decade.

“We lost 3 million during COVID alone, then another 3.7 million during the supply chain crisis,” he continued. “Cumulative sales losses are 16.1 million over the past decade, nearly matching our forecast for the year.

“In short, the industry has lost an entire year’s worth of new-vehicle sales over this past decade,” Jominy went on to state.

And perhaps in a twist, as those sales are declined, prices have rocketed higher.

Catalyst IQ data shows average marketed price (AMP) is approaching an all-time high, reaching $51,610 on May 26, just

Over the past year, AMP increased by $1,896 with almost 85% of that growth taking place since March 1 alone. Coupled with affordability pressures, higher interest rates, and fuel prices approaching all-time highs—up more than $1.50 per gallon over the past eleven weeks—this rapid price growth is creating additional challenges for dealers entering the summer selling season.

“Historically, rising new-vehicle prices have created tailwinds for used demand as affordability-conscious consumers shifted into pre-owned inventory. That dynamic still appears to be playing out today, but with important limitations,” Wainschel told Cherokee Media Group.

Through a separate news release, Wainschel gave more insight through the prism of new models.

“Historically, higher vehicle prices were often temporary and corrected quickly through incentives or discounting,” Wainschel said. “This shift is fundamentally different for the industry. Several of the most profitable vehicle categories — including full-size trucks, full-size SUVs, heavy-duty trucks, and luxury midsize SUVs — are reaching all-time highs. These MSRP-driven price increases are resetting long-term pricing levels, making them more difficult to reverse.”

Catalyst IQ then explained this environment creates both opportunity and risk as consumer shopping behavior is influenced unevenly across segments, geographies, and vehicle configurations.

“It comes down to understanding where demand remains resilient and looking for pockets where affordability resistance is emerging,” Wainschel said. “Dealers who understand that every segment, trim and brand behaves differently in this market will be the ones who are successful in keeping business steady and earning customers’ business as they navigate current economic conditions.”

Easier said than done, right? Well, Catalyst IQ offered a few recommendations in a blog post that accompanied its data.

Here are six strategies Catalyst IQ suggested for dealerships operating in this higher-priced market.

- Audit price position, then act surgically

“As pricing rises, not every VIN requires the same strategy. Use VIN-level market intelligence to identify which vehicles remain competitively positioned and which are beginning to face price resistance. Protect margin where demand supports it, while making targeted adjustments only where needed.”

- Use lower-priced new, used, and certified inventory as affordability release valves

“As vehicle prices climb, a focus on more affordable models and trims informs consumers that there are still accessible choices to consider (see list below*). Additionally, used and certified inventory can become increasingly important alternatives for payment-sensitive shoppers. Dealers that strategically position vehicles that are within the means of a larger proportion of consumers can be better positioned to preserve volume and retain consumers who are stretching on affordability.”

- Protect volume by strengthening top-of-funnel visibility

“In higher-priced segments, shoppers often take longer to make decisions and compare more options before converting. Maintaining strong upper-funnel visibility helps ensure your dealership stays in the consideration set without relying too heavily on broad discounting.”

- Rebuild the message around total value, not just sticker price

“As affordability pressure increases, consumers look beyond monthly payments alone. Reinforce ownership value, capability, warranty coverage, fuel efficiency, and real-world usefulness consistently across digital advertising and vehicle detail pages.”

- Expand reach selectively based on demand signals

“Broader geographic or platform expansion can create opportunity, but only when supported by data. Use localized demand and inventory insights to identify where incremental reach is most likely to drive efficient results.”

- Monitor market resistance and adjust quickly

“In a fast-moving pricing environment, conditions can shift rapidly by segment, geography, and even individual configurations. Dealers that regularly evaluate pricing position, demand signals, and inventory efficiency will be better positioned to respond before resistance turns into aging inventory and wasted spend.”

EV Buyers Keep Trading In Gas Cars Despite Higher Prices

Posted Monday, June 1, 2026

There’s no Federal EV tax credit incentive anymore, but more buyers are switching anyway – from 67.1% in January to 72.1% in April.

Key Points

- EV trade-ins rose from 67.1% in January to 72.1% in April.

- Used EV prices increased 11% this year, outpacing non-EVs for six weeks.

- If this trend continues, then we might be seeing a real trend away from gasoline power.

Moving to Electric

According to data from Edmunds, the shift from gas to electric has increased from 67.1% in January this year to 72.1% in April; this is the rate at which EV buyers are trading in their gasoline-powered vehicles, even without federal tax incentives.

The increase suggests that more and more people are making the switch, and a sustained rise over the next few months will indicate a significant shift in the market towards electric power.

Trend or Fad?

There are numerous factors to consider here. Electric power has recently proven itself to be a hedge against rising gas prices. Current electric vehicle owners have been able to skip the pump entirely, opting to charge at home or at nearby fast chargers. That’s just one of the driving factors forcing car buyers to switch.

Looking at the other numbers, we saw that 26.2% of buyers in January traded in an old EV for a new one. That EV-to-EV trade-in rate has since risen to 35.4% in April. Furthermore, the removal of the $7,500 Federal EV tax credit incentive has soured the deal, but consumers are still going through with their purchases. So, can we say that this is a real trend and that EVs have real momentum?

Used Car Prices on The Rise

Everything is getting more expensive, but even more so on the EV side. Brand-new cars are getting more expensive as costs rise, and it gets harder and harder to do business. Importation costs have inflated price points. However, that also extends to used cars, including EVs. Lower running costs are also part of the equation here. No engine means no fuel is needed, and motor oil is also seeing a price bump as raw material supply gets strained.

From Cox Automotive, “we continue to see EV prices rising faster and holding higher than non-EVs. Three-year-old EV prices have outpaced non-EVs for six weeks in a row and are 11% higher than they were at the start of the year. The longer gas prices remain elevated, the more we expect consumers to turn to fuel-efficient vehicles. As EV lease maturities come to increase throughout the summer, it will be critical to follow EV price trends – especially if the Middle East conflict remains unresolved,” said Jeremy Robb, Chief Economist at Cox Automotive.

Gas-guzzling SUVs didn’t see as large an uptick as used EVs, with the rate rising by just 0.3% since last year. Again, this can be attributed to the gas crisis we’re currently facing.

However, compact gasoline cars, which are more fuel-efficient, saw the second-highest increase behind used EVs, at 7.6%. Because of that, one could infer that it’s more about the running fuel costs than a full-on transition to electric power.

Source: AutoBlog

What's New -May 2026

Posted Thursday, April 30, 2026

Auction sales reach highest level in nearly 6 years

Posted Thursday, April 30, 2026

7-year car loans grows as buyers ‘work harder to make the numbers fit,’ expert says

Posted Thursday, April 30, 2026

- The share of car buyers in the first quarter who signed a loan for 84 months or longer reached about 23%, up from 10% a decade ago, Edmunds data shows.

- The share of new-car buyers with annual income below $100,000 was 37% last year, down from 50% in 2020, according to Cox Automotive.

- Depreciation can lead to being “underwater” on the loan, which can lead to carrying that so-called negative equity into a new car loan if you trade it in.

For a growing share of car buyers, paying for a vehicle is a seven-year commitment.

A record 22.9% of financed new-car purchases in the first quarter involved loans of at least 84 months, according to new data from car shopping and research site Edmunds. That’s up from 21.2% a year prior. A decade ago, it was 10%.

The average amount financed for new cars also reached a record high, climbing to $43,899 in the first quarter, up from $41,473 a year earlier, Edmunds data shows.

As the amount continues to climb, “consumers are having to work harder to make the numbers fit — a clear sign of how strained affordability has become,” said Jessica Caldwell, Edmunds’ head of insights.

Average sticker price staying above $50k

The average sticker price on a new car in March reached $51,456, marking the 12th consecutive month that it’s been above $50,000, according to Kelley Blue Book. The average transaction price after incentives was $49,275, up 3.5% from a year earlier.

That amount is “reflective of a market that favors large, expensive vehicles,” said Erin Keating, an executive analyst for Cox Automotive.

The share of new-car buyers earning less than $100,000 was 37% last year, down from 50% in 2020, according to Cox Automotive.

‘Think twice’ about a seven-year loan

Higher vehicle prices come as many households have been clobbered by ongoing high inflation that has yet to settle down to the Federal Reserve’s target of 2%. The consumer price index, a key inflation measure, rose 3.3% in March from a year earlier, according to the U.S. Bureau of Labor Statistics’ latest reading, released Friday. That’s up from 2.4% in February.

For car buyers whose budgets need to accommodate higher costs in many areas, stretching out their auto loan for as long as possible may be the only way to afford the payments, said Matt Schulz, chief consumer finance analyst at LendingTree.

“For a lot of people, it’s all about the monthly payment, but the extra cost for financing that car for seven full years is really high,” Schulz said.

“Generally speaking, a seven-year auto loan is something that you really need to think twice about because it’s so expensive,” Schulz said. “If the only way you can afford that vehicle is to finance it for seven years, it may be worth thinking about whether you may be buying a little too much car for you.”

To illustrate the cost of financing: A $43,899 loan at 6.9% — the average in the first quarter, Edmunds found — for 84 months would result in a monthly payment of $660 and would cost you $11,575 in interest over the full life of the loan, according to Bankrate’s auto loan calculator.

A five-year loan (60 months) at the same rate would mean paying $8,132 in interest over the life of the loan — $3,443 less. But the monthly payment would jump to $867.

If you don’t have good credit, the interest rate you’re charged is higher. By way of example: To finance that same amount ($43,899) for 84 months at 13.17% — a recent average rate for borrowers with a credit score of 501 to 600, according to Bankrate — the monthly payment would be $803, and the interest paid over the life of the loan would be $23,525.

And, typically, the longer the loan, the higher the interest rate, Schulz said.

Of course, other factors are considered in the lending decision, including your income, employment and existing debt, as well as how much of your income the monthly payments would eat up.

Depreciation can lead to being ‘underwater’ on your loan

Because of how quickly new cars depreciate, Schulz said, there’s a risk of being “underwater” on your loan fairly quickly when you opt for a longer repayment term. That is, you owe more on the car than it’s worth, also known as negative equity. New cars typically lose about 20% of their value in the first year after purchase and about 55% over five years, according to Kelley Blue Book.

When consumers trade in a car with negative equity, that balance typically gets rolled into a loan for the new car. That larger balance can make it more likely that a buyer will choose a longer loan.

About a third of buyers owe more than their trade-in is worth and roll the remaining amount into the loan on their new car, according to JD Power. That share is similar to pre-pandemic behavior.

About 40.7% of new-vehicle purchases involving negative equity are now financed with 84-month loans, according to Edmunds data.

Source: CNBC

Car-Mart closing 42 more stores

Posted Thursday, April 30, 2026

Last Tuesday marked the end of the road at another 42 buy-here, pay-here dealerships operated by America’s Car-Mart.

Car-Mart president and chief executive officer Doug Campbell explained in a letter to shareholders that the company shuttered 31% of its store footprint that impacted about 18% of its outstanding customer base that is part of its $1.5 billion portfolio of outstanding receivables.

“We did not make this decision lightly and are taking these steps because they are the right thing to do for the long-term health of this business,” Campbell said in that letter about the move approved by Car-Mart’s board on April 7. “Our approach is to preserve liquidity and protect the runway this business needs to reach a sustainable outcome. This includes carrying less inventory than we would in a normalized operating environment and tightening underwriting standards, both of which will result in reduced origination volumes in the near term.

“We will continue to evaluate our entire store portfolio and will take additional action where needed,” he continued. “These are deliberate trade-offs designed to responsibly manage our capital position until additional financing is secured.”

In January, Car-Mart wound down operations at 13 locations after beginning a footprint reduction in November.

Campbell reiterated Car-Mart’s three priorities going forward include:

Protect the company’s servicing and collections infrastructure

“Our approximately $1.5 billion finance receivables portfolio generates significant monthly cash collections,” Campbell said. “Maintaining the teams, technology, and processes that service these accounts is our highest priority.

—Keep cost structure in alignment with the company’s current scale

“The store closures and support staff reductions are designed to do exactly that,” Campbell said.

—Continue to pursue a warehouse credit facility or other revolving asset financing

“To this end, we have engaged with additional potential warehouse lenders,” Campbell told shareholders.

Car-Mart still has more than 90 rooftops in its footprint that’s concentrated in Arkansas, Oklahoma, Texas and Missouri.

“I believe in this business because our customers need transportation and financing,” Campbell said. “Our associates are committed to serving our customers and communities every day.

“The buy-here, pay-here model is durable, and the credit quality improvements we have built over the past two years are real,” he added. “The actions we are taking are designed to protect what we have built and position Car-Mart for the future.”

Source: Autoremarketing

The 10 Vehicles Most Likely To Get Stolen In The US

Posted Thursday, April 30, 2026

Chevrolet

There's no shortage of "these are the most stolen cars" articles, and they're usually grounded in research by the National Insurance Crime Bureau. The problem with these lists is that the NICB is looking at aggregate theft data (that is, how many of each model are stolen across the country in a year). There are certainly trends to observe — the organization has been keeping an eye on the Hyundai/Kia situation for years — but while a vehicle could top the list by being a laughably stealable security risk, it can also get there by being a Honda Accord, which took the No. 2 spot (between two Hyundais) on the NICB list in 2025 despite having no widely recognized security vulnerabilities. There are just a whole lot of Accords out there, so a whole lot of Accords get stolen.

A new study from the Highway Loss Data Institute (HLDI), published via the Insurance Institute for Highway Safety (IIHS), flips that script by measuring thefts relative to how many of each vehicle actually exist. The result is a look at vehicle thefts through a whole new lens, with the top 10 including few of the perennial "hottest car" list favorites. There are no hilariously vulnerable Kias or Hyundais, no relentlessly common Hondas or Toyotas, and not a punchline of an Altima to be found. So sit back, scan your block for nefarious car thieves, and find out if it's time to buy The Club for your ride.

10. Ram 1500 Crew Cab Short Wheelbase 4WD

This is just the 10th most stolen vehicle on the list, but we're going to point out a trend that will pop up a few times before we're done. Four-wheel-drive crew cab pickups are in danger.

The combustion-powered Ram 1500 is surprisingly complicated, with its various drivetrain and cab configurations spread out over 10 trim packages, from the humble Tradesman to the illustrious Tungsten, which carries an $88,800 suggested price before options and $2,595 destination charge. We bring that up just to point out that modern workhorse pickup trucks can also carry borderline luxury energy, with price tags to match. The infotainment screens alone have proven irresistible to thieves, and while that doesn't contribute to the theft totals we're discussing today, it does demonstrate that the bad guys have an eye on the Rams.

They also have the key fobs. Or at least clones of them. Like the compromised Mercedes cars in "Gone in 60 Seconds," in recent years hundreds of vehicles across multiple states have been boosted by a handful of criminals who managed to make their own copies of Dodge fobs, including those of the Ram 1500. To add insult to injury, they then dumped their ill-gotten autos on the illicit market for as low as $3,500. Anyway, before we move on, here's how to protect yourself from keyless car theft.

9. Land Rover Range Rover 4WD

First of all, as part of our ongoing public service education work, we'll point out that Range Rover is a subbrand of Land Rover, which is a subbrand of Tata motors. It's a little confusing, but necessary if you want to accurately point fingers about an ongoing security vulnerability that left its $100,000-plus luxury SUVs vulnerable to being stolen after having their key fob signals intercepted over the air. The result was a $20-million effort announced in 2023 to roll out software updates and work with affected owners to get them installed.

But here's the thing. That whole mess was limited to vehicles manufactured between 2018 and 2022, with the problem resolved under a new electronic architecture in place since. So while no manufacturer wants to show up on a list like this, it probably stung especially in the case of Land Rover. We mean Range Rover. No, Jaguar Land Rover (JLR), wholly owned subsidiary of the Tata Group. That's because the model years that showed up in the new HLDI data ran from '22 to '24, firmly in what Land Rover calls its "resilient to theft" era. Better luck next year?

8. Dodge Durango 4WD

As Durango Hellcat owners lose their lawsuit over their "limited edition" vehicle investments, we've kind of formally adjudicated that treating your Durango as a collector's item isn't a great idea. But that doesn't mean it isn't an attractive theft target.

Matt Moore, chief insurance operations officer at HLDI and IIHS, points out that "Muscle cars have often topped this list, as thieves are attracted to vehicles with high horsepower." And while maybe car thieves are scoping up Durangos because of impressive towing capacity and pleasantly surprising infotainment system, it's also possible that it has to do with the Durango being what Car & Driver describes as "the closest thing to a three-row muscle car," even if you don't opt for the definitively-not-collectible Hellcat edition.

Oh, it doesn't really help that you can carefully remove the windshield from the outside and then program a new key fob on the spot, as some folks in Pennsylvania discovered when they came outside to their Durangoless windshield lying thoughtfully (and unhelpfully) on the ground. As additional evidence of key fob vulnerabilities, a couple of guys in Michigan are accused of stealing more than 25 Durangos right off of dealership lots. Evidently, the criminal underbelly yearns for a powerful three-row SUV.

7. Chevrolet Silverado 3500 Crew Cab 4WD

See? We told you 4WD crew cabs weren't safe. The Chevrolet Silverado HD is built to tow and haul, but that won't do you much good if you come outside to an empty parking spot (or two; we see how some of you animals park these things). While it's possible this is simply more evidence of highly capable heavy-duty American trucks getting plucked for their utility, there's also some evidence that General Motors has a key fob issue of its own, with a whole bunch of Silverados and (spoiler alert for the next entry on our list) GMC Sierras ending up stolen and headed to Mexico using electronic security compromises similar to the ones that have come up already.

Vulnerabilities aside, the 3500 Crew Cab 4WD compares well to the more entry-level Ram we began with above. This is a serious work truck and thieves are apparently going quite deep into the more capable end of Chevy's lineup — these start at $53,595 plus $2,795 destination charge, and can easily exceed $75,000 before options with the High Country variant.

When it comes to the key fob attacks, there's presumably not much different in terms of effort when you jump from the base model Silverado to something like this, so maybe it's not that surprising, but it's still a little fun to think about the apparently plausible scenario of some black-market truck buyer weighing how much extra he's willing to pay for one with the Duramax 6.6 that can tow 36,000?pounds (of additional stolen merchandise, perhaps?).

6. GMC Sierra 3500 Crew Cab 4WD

If you really know what you're doing, you can walk up to a GMC Sierra 3500, disable the horn through the grill (and thus kill the alarm noise), and make off with the truck in under three minutes. That's just one super-specific example of a wider trend in GMC truck thefts, and it wouldn't be a crazy leap to assume there's some overlap with the electronic vulnerabilities already established under the General Motors umbrella with the Chevys discussed already.

From a GM brand standpoint, it's maybe worth an internal PowerPoint slide somewhere that the Sierra 3500 and the Silverado 3500 — product portfolio siblings with essentially identical underpinnings — landed right next to each other in the HLDI data. Perhaps at the end of the day people actually aren't that discriminating when it comes to what badge you slap on the front, at least not if you're just hustling out of the suburbs and across the southern border. Anyway, did we mention that a version of the GMC Sierra 3500 HD now starts at over $100,000?

5. Acura TLX 2WD

We don't really know what to say about this one. Acura killed the TLX after only selling 7,478 of them in 2024 and apparently a good chunk of them were stolen anyway. Together with the even higher-ranking 4WD TLX, you'll notice that the Acura is the only sedan on today's list. Even if you zoom out to the top 20, you'll still only find one other, the Mercedes-Benz S-Class (long wheelbase) down in the 18th spot — and still with the caveat that we're talking about relative theft frequency. A long-wheelbase S-Class isn't exactly a Ford F-150 in terms of sales volume.

Anyway, there doesn't seem to be an obvious, widely documented smoking-gun behind TLX theft rates. The National Highway Traffic Safety Administration previously exempted it from federal parts-marking requirements after concluding its standard immobilizer-based anti-theft system was likely to be effective. But there isn't a specific vulnerability stemming from that, so your guess is probably as good as anybody's.

4. GMC Sierra 2500 Crew Cab 4WD

This is, mercifully, the last of the pickups on this list. Even though the other GM variants we've already discussed share the same vulnerabilities and ultimately the same fate, this is the model that made the biggest media splash in the "they're comin' for your pickups" genre of local news. That said, expensive, work-focused trucks surely seem to remain highly desirable in illicit markets.

Like its smaller sibling, the 1500, you can push these quite high in terms of suggested price with the available Denali packages, except in this case the Denali Ultimate can get you all the way up to $94,200 before options and $2,795 destination charge.

But for those of you who enjoy some rampant speculation to go with their data-driven actuarial analysis of insurance data, we'll at least attempt to oblige. Based strictly on the data set, the off-roading GMC Sierra 2500 HD AT4X falls under the "GMC Sierra 2500 Crew Cab 4WD" umbrella, meaning that we can't say that these theft numbers aren't driven purely by the enthusiasm of nefarious characters who simply appreciate the awesome capability of one of the coolest all-terrain trucks you can buy from the factory. So maybe it's that? (It's probably not that.)

3. Chevrolet Camaro

Finally! We were getting a little frustrated with that HLDI guy we quoted back in the Durango section, who promised muscle cars before providing nothing but pickup trucks and an Acura sedan ever since — until now. The (since discontinued) Chevy Camaro marks a shift into performance territory, with a look and feel finally worthy of Grand Theft Auto opening the door to, well ... grand theft auto.

So why a Camaro and not a Mustang, or maybe one of those Challengers with the lip guard still on the front splitter? It's that key fob vulnerability again. GM issued a recall (sorry, we mean "customer satisfaction program") on this one, offering a body control module update after some areas reported Camaro thefts spiking more than 1,000%, directly attributable to key fob cloning, sometimes perpetrated by literal children.

Except this time, instead of snatching signals out of the air or gaining access to an actual fob, thieves are managing to pull key codes directly from the OBD-II port, taking advantage of a diagnostic interface that really probably shouldn't include access to that sort of thing. So since we're not sure if the Camaro will ever come back as a Chevy offering, you might want to go out of your way to keep yours safe if you have one.

2. Acura TLX 4WD

You didn't lose your place. It's a slightly different TLX. The Acura TLX 4WD has doubled up Acura near the top of our list here, and it's frankly kind of annoying that the HLDI made this distinction between the two drivetrains. There are no obvious security exploits or electronic vulnerabilities that apply to the 4WD as compared to the 2WD and really the story here is that people want these Acura sedans badly enough to steal them, yet not enough to purchase them in sufficient volumes to keep them in the lineup. All that said, we did put some thought into what might be at least a contributing factor for what's going on here and didn't come up completely empty-handed.

This entry in the data would include the Type S. The Acura TLX Type S is a different kind of AWD sport sedan. It has performance that's Machines With Souls compared to "a four-door NSX," and if that doesn't at least put it into the sports car conversation with a base model Camaro, we're not sure what does.

But importantly, every Type S is all-wheel drive, meaning that if (big, big if, to be clear) would-be car thieves are looking for a high-performance good time, perhaps with some legendary Japanese reliability, then they might opt for a TLX Type S, and in doing so boost the theft rate reflected in the "Acura TLX 4WD" data. It's a theory, anyway. Call us next time you want to dig into the story behind the story, HLDI.

1. Chevrolet Camaro ZL1

(Boss music plays.) Putting a satisfying bow on this whole data-driven exercise, it's the Camaro ZL1. It's exactly the kind of vehicle that gets overlooked in the usual "most stolen cars" lists because there simply aren't that many of them, and frankly it's a little bit fun to imagine Nicolas Cage doing a "Gone in 60 Seconds" reboot that includes tearing off in a 650-horsepower supercharged V8 hero car with a manual transmission for those quick cinematic shots from inside the pedal box.

The ZL1 has all of the same security vulnerabilities as the base model Camaro we covered earlier, plus the fierce looks and exceptional performance that make it an icon worthy of risking jail time. Taken together, the result is that the Chevy Camaro ZL1 is 39 times more likely to be stolen than the average car and gaps the competition in taking its spot at the top of this list. Well done, Chevy. If only you'd keep making 'em.

Source: Jalopnik